All Categories

Featured

Table of Contents

[/image][=video]

[/video]

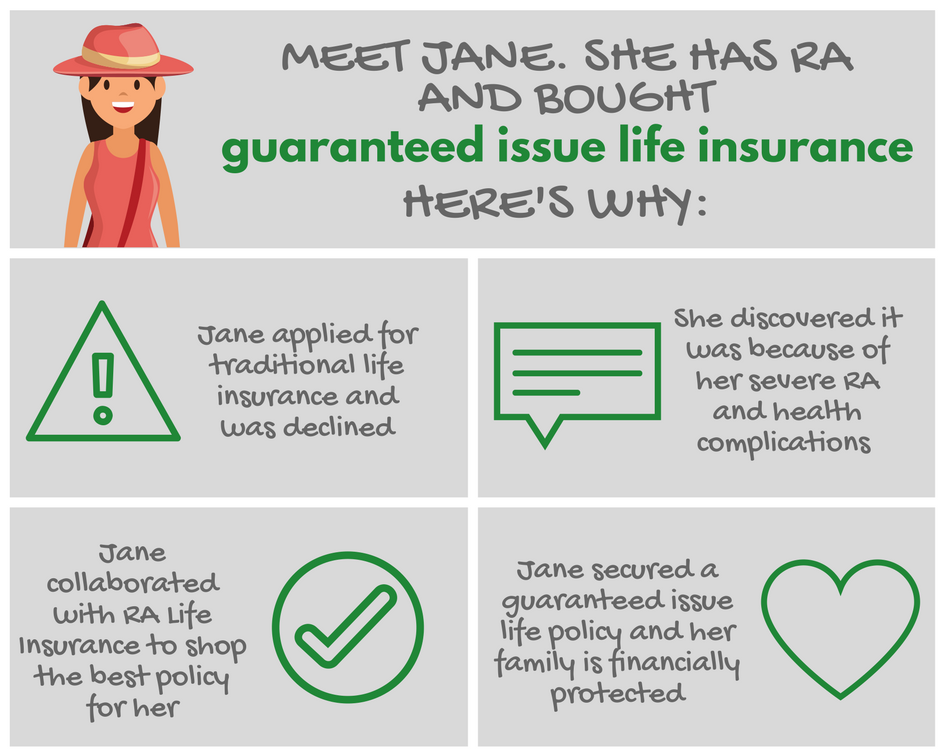

If you remain in healthiness and happy to undergo a medical test, you may get approved for standard life insurance at a much reduced expense. Surefire concern life insurance is often unnecessary for those healthy and can pass a medical examination. Since there's no clinical underwriting, also those in excellent wellness pay the same costs as those with wellness concerns.

Given the reduced coverage quantities and higher premiums, assured problem life insurance policy may not be the best alternative for long-lasting economic preparation. It's often extra suited for covering last expenditures instead than changing revenue or considerable financial debts. Some guaranteed problem life insurance policy plans have age constraints, often restricting candidates to a certain age array, such as 50 to 80.

Assured issue life insurance policy comes with greater premium prices contrasted to clinically underwritten plans, yet prices can differ substantially depending on factors like:: Different insurance policy companies have various prices designs and may offer various rates.: Older applicants will pay higher premiums.: Women frequently have reduced prices than men of the very same age.

: The survivor benefit quantity affects costs. A $25,000 plan expenses much less than a $50,000 policy.: Paying costs monthly costs extra total than quarterly or annual payments.: Entire life premiums are greater overall than term life insurance coverage plans. While the ensured concern does come with a rate, it provides vital coverage to those who might not get approved for traditionally underwritten policies.

Guaranteed problem life insurance policy and simplified issue life insurance policy are both kinds of life insurance that do not need a medical examination. Nevertheless, there are some essential differences between the 2 kinds of policies. is a kind of life insurance policy that does not require any type of wellness concerns to be addressed.

What Is Instant Life Insurance? Things To Know Before You Get This

Guaranteed-issue life insurance policy policies commonly have higher premiums and reduced fatality benefits than conventional life insurance policy policies. The wellness concerns are normally much less comprehensive than those asked for conventional life insurance policy plans.

Immediate life insurance protection is protection you can get an instant response on. Your policy will certainly start as soon as your application is approved, implying the whole procedure can be done in less than half an hour.

Instant insurance coverage only applies to label plans with accelerated underwriting. Second, you'll require to be in excellent health and wellness to certify. Numerous internet sites are promising split second insurance coverage that starts today, yet that doesn't imply every candidate will certify. Typically, customers will submit an application assuming it's for instant coverage, only to be met a message they require to take a medical examination.

The same info was after that utilized to authorize or reject your application. When you apply for a sped up life insurance policy plan your information is examined instantly. A computer algorithm analyzes the data from your application along with details concerning you from credit rating reporting agencies, the DMV, the Medical Info Bureau, and data solutions like LexisNexis.

You'll then obtain instant authorization, instant rejection, or observe you need to take a clinical examination. There are several choices for instant life insurance policy.

The Best Guide To Aarp Guaranteed Life Insurance From New York Life

The firms below offer totally on-line, easy to use alternatives. The company uses flexible, instantaneous plans to people in between 18 and 60. Ladder plans permit you to make adjustments to your insurance coverage over the life of your plan if your demands alter.

The business uses policies to applications between 21 and 55 for a ten-year term, and between 21 and 45 for a 20-year term. Ethos policies are backed by Legal and General America.

Much like Ladder, you might require to take a medical test when you look for insurance coverage with Ethos. The company claims that the bulk of applicants can get protection without an exam. Unlike Ladder, your Values policy won't begin right away if you require an examination. You'll need to wait till your examination outcomes are back to obtain a cost and get protection.

In other instances, you'll need to provide even more information or take a medical exam. Below is a price contrast of insant life insurance policy for a 50 year old man in good health.

Many individuals begin the life insurance acquiring plan by getting a quote. Let's state you obtained a quote for $50 a month for a $500,000, 20-year plan.

You can establish the specific protection you're using for and after that start your application. A life insurance policy application will ask you for a lot of details.

Some Known Details About Dave Ramsey-recommended Affordable Life Insurance

It is very important to be 100% sincere on your application. If the business finds you really did not divulge information, your policy could be denied. The decrease can be mirrored in your insurance rating, making it more challenging to obtain insurance coverage in the future. As soon as you submit your application, the underwriting algorithm will analyze your info and pull information to come to an immediate choice.

A simplified underwriting policy will certainly ask you in-depth inquiries about your clinical history and current medical care during your application. An instantaneous problem plan will do the very same, yet with the distinction in underwriting you can get an immediate decision. There are numerous differences between surefire issue and immediate life insurance.

And also, guaranteed problem policies aren't able to be used throughout the waiting duration. For the majority of plans, the waiting duration is 2 years.

Yes. If you're in excellent health and wellness and can qualify, an instant issue policy will certainly allow you to get insurance coverage without any exam and no waiting period. What happens if you remain in much less than perfect health and wellness and want a policy with no waiting duration? In that case, a simplified problem plan with no exam might be best for you.

Unknown Facts About Life Insurance Without A Medical Exam

Bear in mind that simplified issue policies will certainly take a few days, while instantaneous policies are, as the name indicates, immediate. Purchasing an instantaneous plan can be a rapid and simple procedure, yet there are a couple of points you must enjoy out for. Before you hit that acquisition switch make sure that: You're getting a term life policy and not an unintentional death policy.

They don't provide insurance coverage for health problem. Some companies will issue you an unexpected fatality plan instantaneously yet require you to take an exam for a term life policy. You have actually checked out the small print. Some internet sites teem with colorful photos and strong pledges. Ensure you read all the information.

Your representative has answered all your questions. Simply like websites, some agents emphasize they can get you covered today without explaining or supplying you the info you require.

{kind=link}

Table of Contents

Latest Posts

Facts About What Is An Instant Life Insurance Policy? Revealed

The 20-Second Trick For The Top 15 No Exam Life Insurance Companies

The Best Cheap Life Insurance Companies Of 2025 Fundamentals Explained

More

Latest Posts

Facts About What Is An Instant Life Insurance Policy? Revealed

The 20-Second Trick For The Top 15 No Exam Life Insurance Companies

The Best Cheap Life Insurance Companies Of 2025 Fundamentals Explained